Online Booking

Online Booking

U.S. Terminates IEEPA Duties, 10% Temporary Tariff Takes Effect Under Section 122

Source: The White House Presidential Proclamation

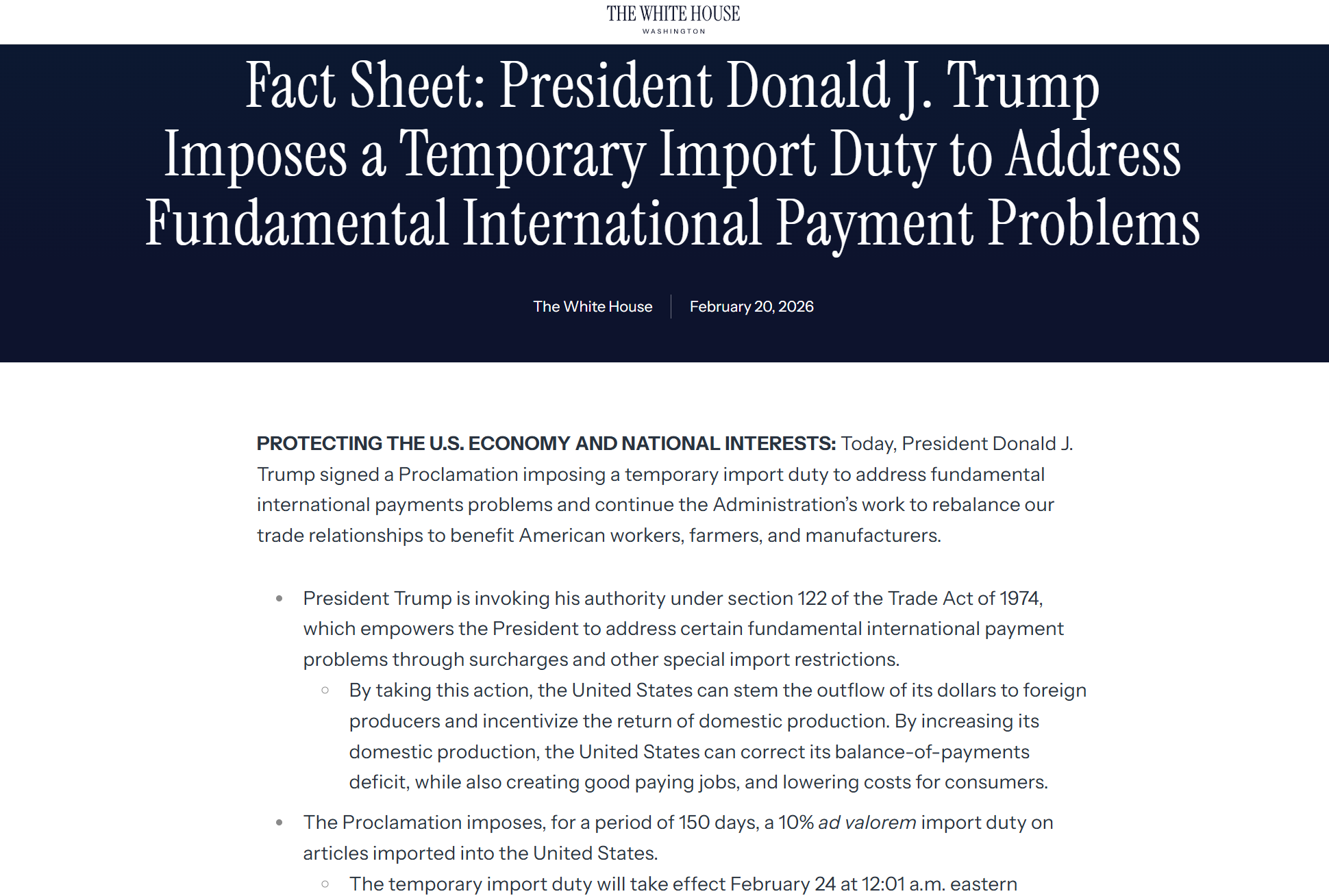

The United States has completed a transition in its import tariff framework. Additional duties imposed under the International Emergency Economic Powers Act (IEEPA) have been terminated. At the same time, the U.S. government has invoked Section 122 of the Trade Act of 1974 to impose a 10% temporary import surcharge.

This marks a shift in legal authority and surcharge structure — not a reduction in overall tariff exposure.

1、Legal Transition and Key Parameters

IEEPA-based duties were formally terminated on February 22, 2026.

On February 23, 2026, a Presidential Proclamation under Section 122 introduced a temporary 10% surcharge.

Key parameters:

- Rate: 10%

- Effective date: February 24, 2026

- Duration: 150 days

- Scheduled expiration: July 24, 2026

The Section 122 surcharge applies in addition to existing Section 301 and Section 232 duties. It replaces IEEPA as the legal basis but does not eliminate layered tariff exposure.

2、Transitional Treatment for Goods in Transit

A limited transition window applies. Shipments qualify only if they:

- Were loaded prior to February 24, 2026;

- Arrive at a U.S. port by February 28, 2026.

Entries outside this window are subject to the 10% surcharge. Shipment timing is therefore critical.

3、Current Tariff Structure for China-Origin Exports

China-origin exports to the U.S. may now face:

- MFN base duties

- Section 301 additional duties

- Section 232 duties (where applicable)

- Section 122 temporary 10% surcharge

The Section 122 measure is additive. For certain product categories, cumulative effective duty rates may increase.

4、Commercial Impact

Key implications include:

- Higher cumulative duty exposure

- Required recalibration of pricing models

- Increased importance of shipment timing

- Margin pressure in low-margin sectors

Industries such as textiles, furniture, home appliances, light manufacturing, and selected electronics may be directly affected where the 10% surcharge compounds existing duties.

5、Operational Considerations

Exporters should focus on:

- HS classification verification

- Full landed cost recalculation

- Tight coordination of shipment schedules

- Review of tariff allocation clauses

- Monitoring potential policy extension beyond July 24, 2026

During this temporary implementation period, disciplined cost modeling and supply chain planning are essential.

6、Implementation Window and Planning

The Section 122 surcharge is scheduled to remain in effect through July 24, 2026. Future extension or modification remains subject to further government action.

TPL will continue monitoring developments and supporting clients with duty analysis, compliance review, and shipment planning to help maintain supply chain stability during this transitional phase.

For product-specific assessments or shipment planning support, please contact our team.